Recent research by the National Association of Realtors (NAR) examined certain red flags that caused the housing crisis in 2005, and then compared them to today’s real estate market. Today, we want to concentrate on four of those red flags.

Price to Rent Ratio

Price to Income Ratio

Mortgage Transactions

House Flipping

All four categories were outside historical norms in 2005. Home prices were way above normal ratios when compared to both rents and incomes at the time.

NAR explained that mortgage transactions as a percentage of all home sales were also at a higher percentage:

“Loose credit was one of the main culprits of the housing crisis. Mortgage lending expanded dramatically as unhealthy housing speculation reached its

Have you ever been flipping through the channels, only to find yourself glued to the couch in an HGTV ‘show hole’*? We’ve all been there… watching entire seasons of “Love it or List it,” “Fixer Upper,” “House Hunters,” “Flip or Flop,” “Property Brothers,” and so many more, just in one sitting.

When you’re in the middle of your real estate themed show marathon, you might start to think that everything you see on TV must be how it works in real life, but you may need a reality check.

Reality TV Show Myths vs. Real Life:

Myth #1: Buyers look at 3 homes and make a decision to purchase one of them.

Truth: There may be buyers who fall in love and buy the first home they see, but more often than not the process of buying a home means touring

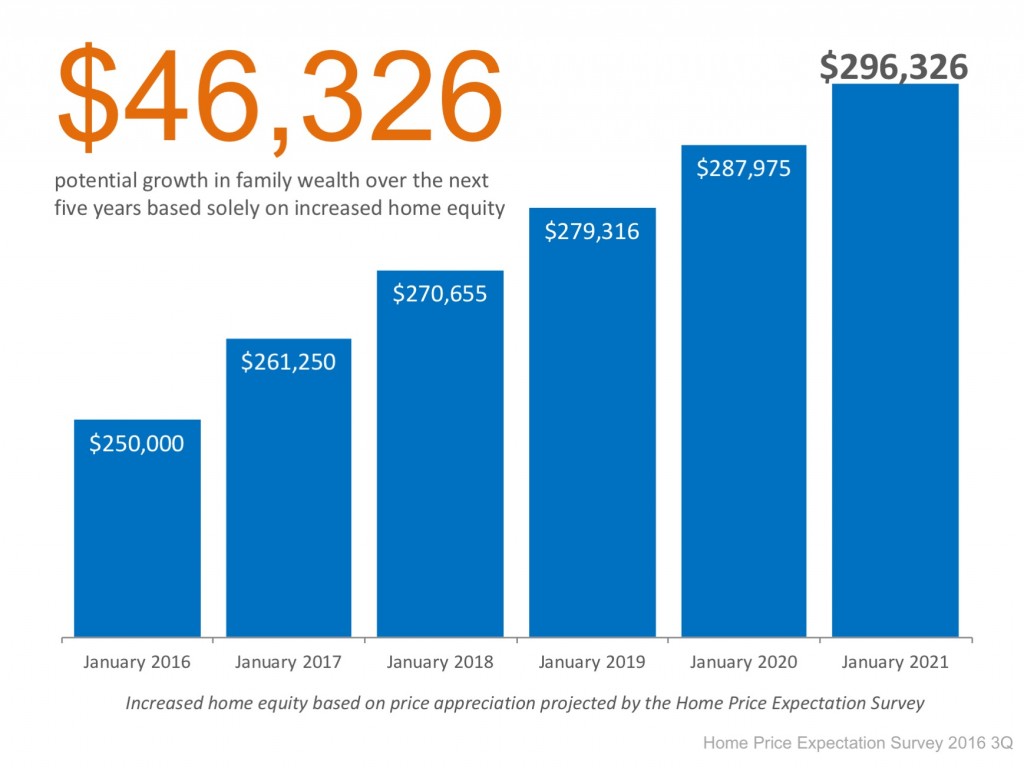

Yesterday, we shared the results of the latest Home Price Expectation Survey by Pulsenomics. One of the big takeaways from the survey is that over the next five years, home prices will appreciate 3.5% per year on average, and cumulatively will grow by around 18%.

So what does this mean for homeowners and their equity position?

For example, let’s assume a young couple purchased and closed on a $250,000 home in January of this year. If we only look at the projected increase in the price of that home, how much equity would they earn over the next 5 years?

Since the experts predict that home prices will increase by 4.5% this year alone, the young homeowners will have gained over $11,000 in equity in just one year.

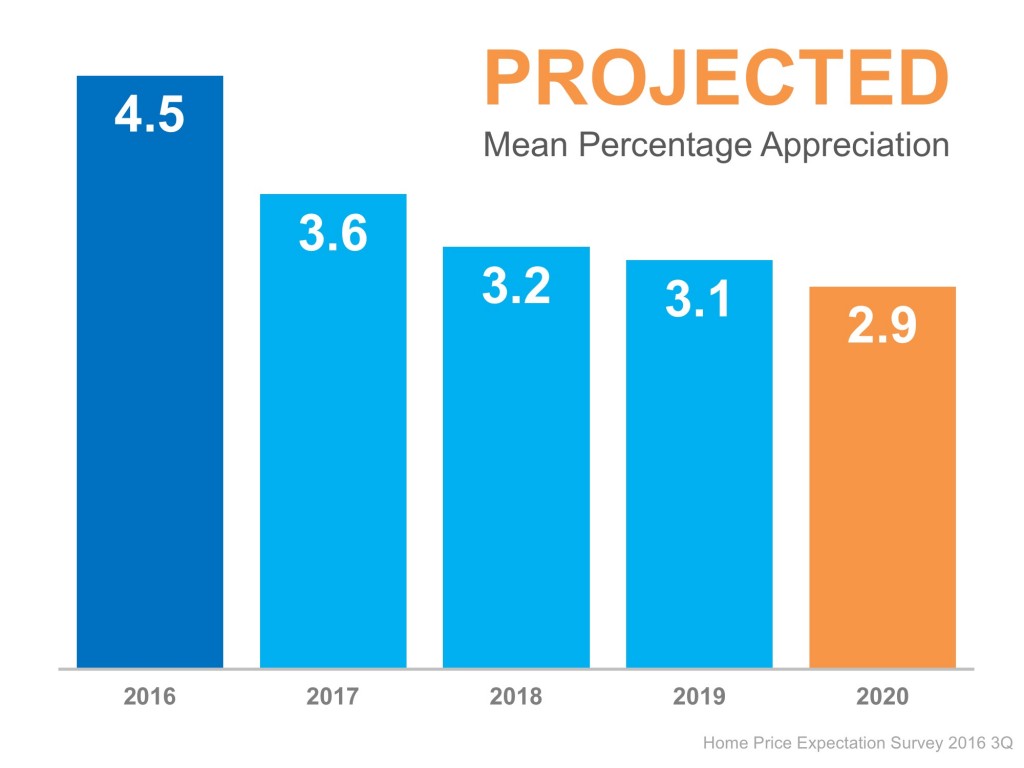

Today, many real estate conversations center on housing prices and where they may be headed. That is why we like the Home Price Expectation Survey.

Every quarter, Pulsenomics surveys a nationwide panel of over one hundred economists, real estate experts, and investment & market strategists about where they believe prices are headed over the next five years. They then average the projections of all 100+ experts into a single number.

The results of their latest survey:

Home values will appreciate by 4.5% over the course of 2016, 3.6% in 2017 and about 3.2% in the next two years, and finally 2.9% in 2020 (as shown below). That means the average annual appreciation will be 3.5% over the next 5 years.

Thinking of moving across the country? How far will your money take you?

The majority of states in the Midwest and South offer a lower cost of living compared to Northeast and Western states.

The ‘Biggest Bang for your Buck’ comes in Mississippi where, compared to the national average, you can actually purchase $115.34 worth of goods for $100.

In a recent post, CoreLogic looked at the correlation between stocks and the sales of upper-end properties ($1 Million+ sales price). The report revealed:

“The powerful ‘wealth effects’ generated by the rapid rise in equities between 2009 and 2015 drove a large rise in the sales of homes that sold for $1 million or more.

Historically, sales of homes priced $1 million or more averaged 1.2 percent of all home sales. The spread between high-end sales and equities widened during the housing bubble but then moved more closely in unison. By the time the equity markets had peaked in May 2015, the $1 million or more share of the market had nearly doubled, averaging 2.2 percent for the remainder of the year.”

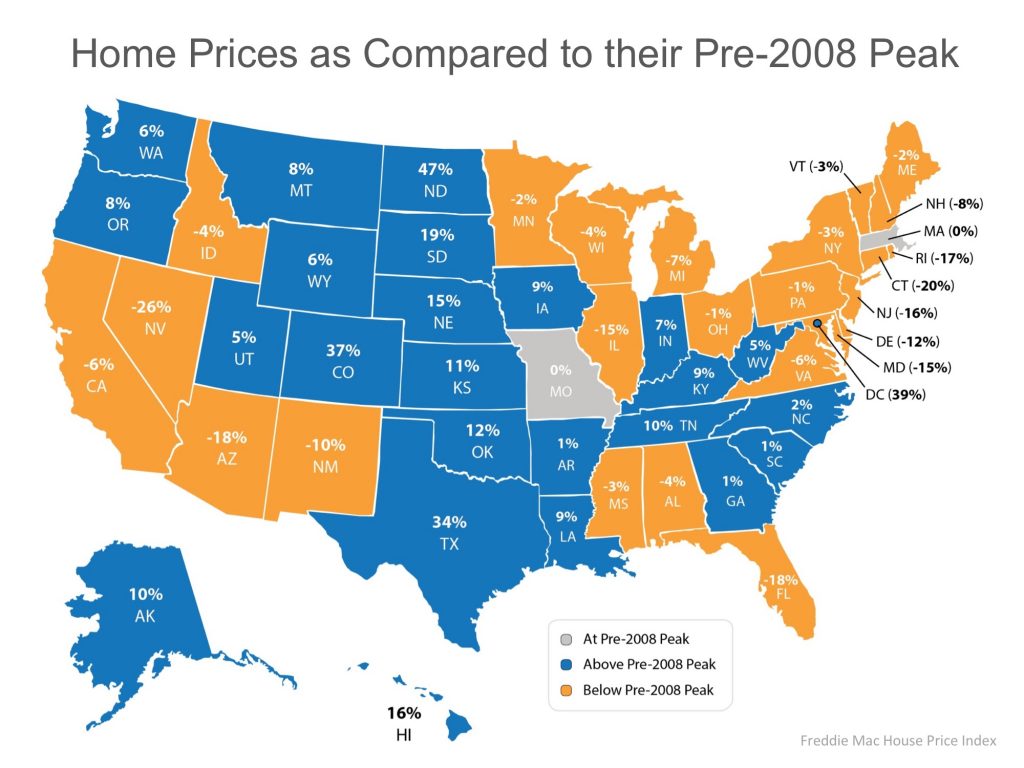

This housing market has many people talking about home values; where they are and where they are headed. It’s also interesting to look back and see how home prices compare to values prior to the housing crisis.

Every quarter, Freddie Mac releases their House Price Index. The index usually provides monthly home values for:

the nation as a whole

each of the 50 states

367 metropolitan statistical areas

This quarter, the report also included a look at today’s home values as compared to Pre-2008 values. Here is a graphic that breaks down the numbers on a state-by-state basis:

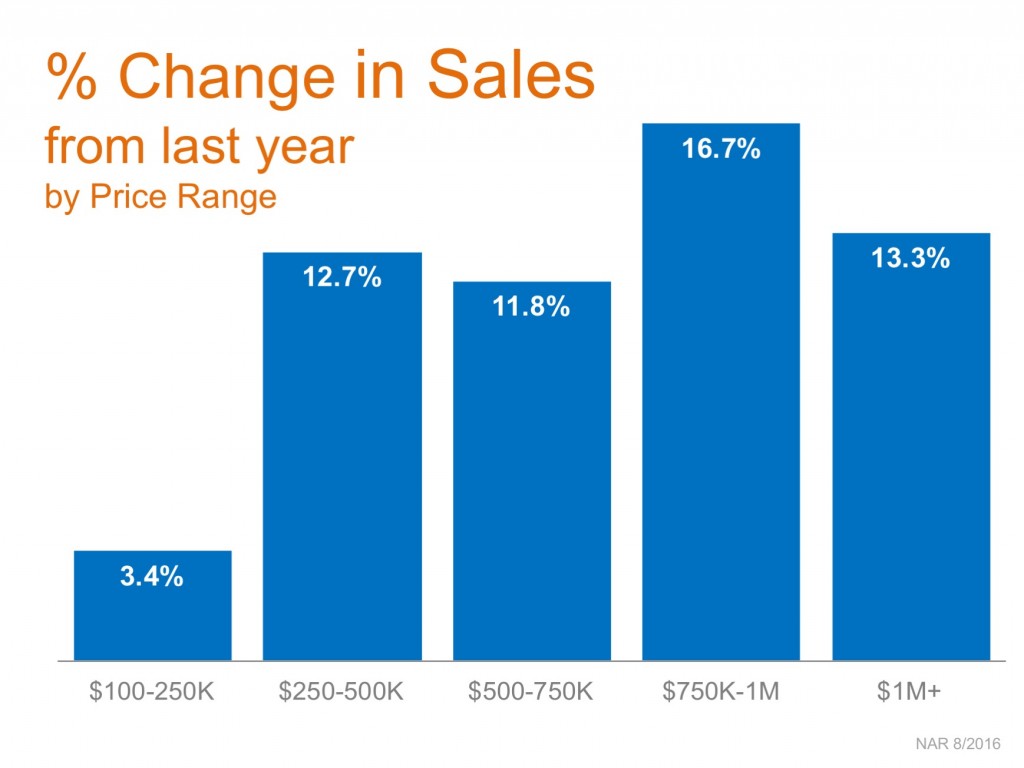

The National Association of Realtors’ most recent Existing Home Sales Report revealed that home sales were up rather dramatically over last year in five of the six price ranges they measure.

Homes priced between $100-250K showed a modest increase at 3.4%. This not only points to the lower inventory of homes available for sale in this price range but also speaks to the overall strength of the housing market.

Sales of homes over $250,000 increased by double digit percentages with sales in the $750,000- $1 million range showing the largest increase, up 16.7%!

As prices in many markets continue to accelerate, it is no surprise to see the percentage of homes in the higher price ranges increasing.

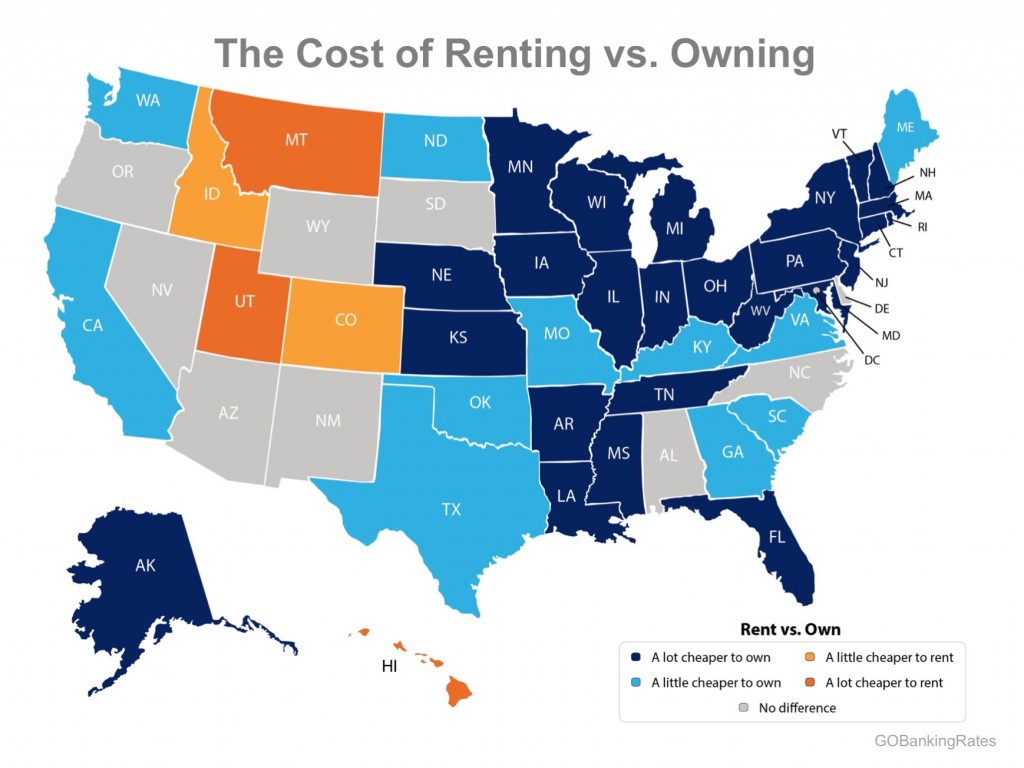

In the latest Rent vs. Buy Report from Trulia, they explained that homeownership remains cheaper than renting with a traditional 30-year fixed rate mortgage in the 100 largest metro areas in the United States.

The updated numbers actually show that the range is an average of 5% less expensive in Orange County (CA) all the way up to 46% in Houston (TX), and 36% Nationwide!

A recent study by GoBankingRates looked at the cost of renting vs. owing a home at the state level and concluded that in 36 states it is actually ‘a little’ or ‘a lot’ cheaper to own, represented by the two shades of blue in the map below.

One of the main reasons that owning a home has remained significantly cheaper than renting is the fact that interest rates have

![‘Old Millennials’ Are Diving Head-First into Homeownership [INFOGRAPHIC] | Simplifying The Market](http://www.simplifyingthemarket.com/wp-content/uploads/2016/08/Old-Millennials-ENG-STM-726x1024.jpg)

![What States Give You the Most ‘Bang for Your Buck’? [INFOGRAPHIC] | Simplifying The Market](http://www.simplifyingthemarket.com/wp-content/uploads/2016/08/20160812-100-Gets-You-STM-791x1024.jpg)