There are some that think that housing affordability is a challenge. Historically, that’s not true. Others think that home prices are approaching bubble values. If we look back over the last sixteen years, that is also not the case. As a matter of fact, the numbers show that the U.S. residential real estate market is doing just fine.

Here are two articles and excerpts that make this point:

The Housing Market Is Finally Starting to Look Healthy – The NY Times

“It has been an excruciatingly long time coming, but the housing sector in the United States is finally getting healthy. Thank millennials and thank homebuilders who are starting to produce more of the starter houses young people demand.”

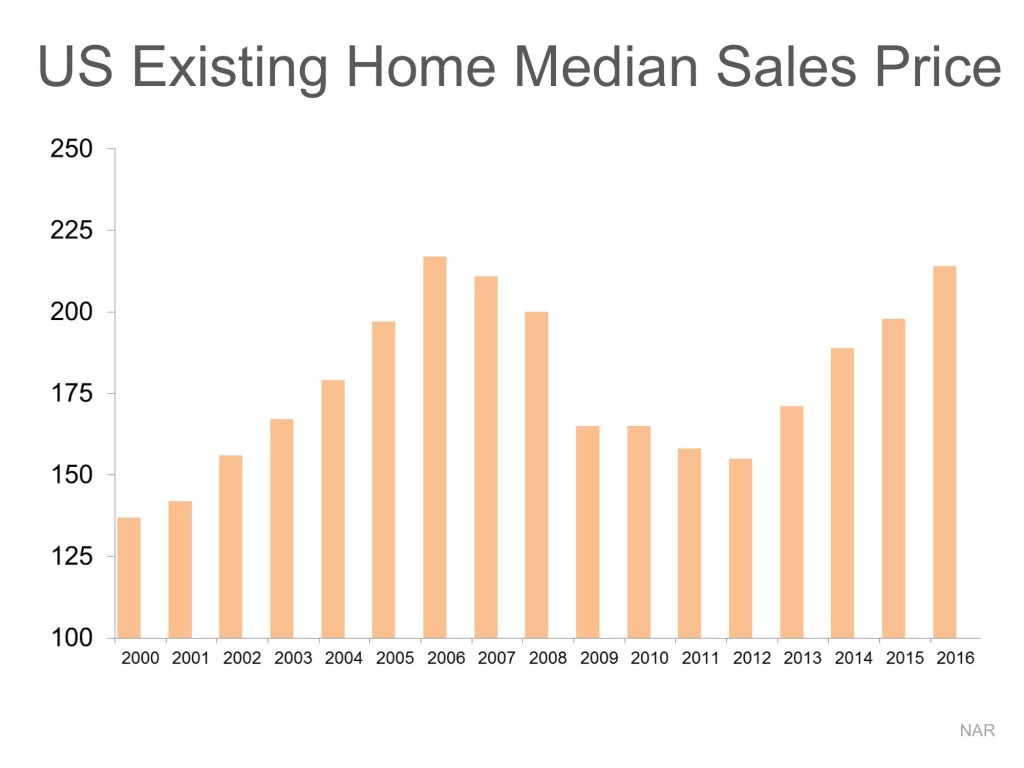

There are some industry pundits claiming that residential home values have risen too quickly and that current levels are on the verge of another housing bubble. It is easy to see how this thinking has taken form if we look at a graph of home prices from 2000 to today.

The graph definitely looks like a rollercoaster ride. And, as prices begin to reach 2006 levels again, it “seems logical” that the next part of the ride would be downhill. However, this graph includes the anomaly of the price bubble and the correction (the housing crash).

What if the bubble & bust didn’t occur?

Let’s assume that instead of the rise and fall in home prices that we saw last decade, we just had normal historic appreciation from 2000 to today. According to the

We are often asked why there is so much paperwork mandated by the bank for a mortgage loan application when buying a home today. It seems that the bank needs to know everything about us and requires three separate sources to validate each and every entry on the application form.

Many buyers are being told by friends and family that the process was a hundred times easier when they bought their home ten to twenty years ago.

There are two very good reasons that the loan process is much more onerous on today’s buyer than perhaps any time in history.

1. The government has set new guidelines that now demand that the bank prove beyond any doubt that you are indeed capable of affording the mortgage.

There are many benefits to homeownership. One of the top ones is being able to protect yourself from rising rents and lock in your housing cost for the life of your mortgage.

Don’t Become Trapped

Jonathan Smoke, Chief Economist at realtor.com, reported on what he calls a “Rental Affordability Crisis.” He warns that,

“Low rental vacancies and a lack of new rental construction are pushing up rents, and we expect that they’ll outpace home price appreciation in the year ahead.”

In the Joint Center for Housing Studies at Harvard University's 2015 Report on Rental Housing, they reported that 49% of rental households are cost-burdened, meaning they spend more than 30% of their income on housing. These households struggle to save for a rainy

Some industry pundits are saying that the housing market may be heading for a slowdown. One of the data points they use is the falling numbers of the Housing Affordability Index, as reported by the National Association of Realtors (NAR).

Here is how NAR defines the index:

“The Housing Affordability Index measures whether or not a typical family earns enough income to qualify for a mortgage loan on a typical home at the national level based on the most recent price and income data.”

Basically, a value of 100 means a family earning the median income earns enough to qualify for a mortgage on a median priced home, based on the price and mortgage interest rates at the time. Anything above 100 means the family has more than enough to

Many experts have been calling upon home builders to ramp up construction to help with the lack of existing inventory for sale. For the past two months, new home sales have surged, with July’s total coming in at the highest since October 2007.

The latest estimates from the US Census Bureau and Department of Housing and Urban Development show that sales in July were 31.3% higher than this time last year, and 12.4% higher than last month, at a seasonally adjusted annual rate of 654,000.

Zillow’s Chief Economist, Svenja Gudell, echoed the reaction of some as she commented:

“July(‘s) new home sales data was a surprise, but a welcome one. For years, the market has been practically begging builders to both ramp up their efforts overall and to

Fannie Mae’s “What do consumers know about the Mortgage Qualification Criteria?” Study revealed that Americans are misinformed about what is required to qualify for a mortgage when purchasing a home.

Myth #1: “I Need a 20% Down Payment”

Fannie Mae’s survey revealed that consumers overestimate the down payment funds needed to qualify for a home loan. According to the report, 76% of Americans either don’t know (40%) or are misinformed (36%) about the minimum down payment required.

Many believe that they need at least 20% down to buy their dream home. New programs actually let buyers put down as little as 3%.

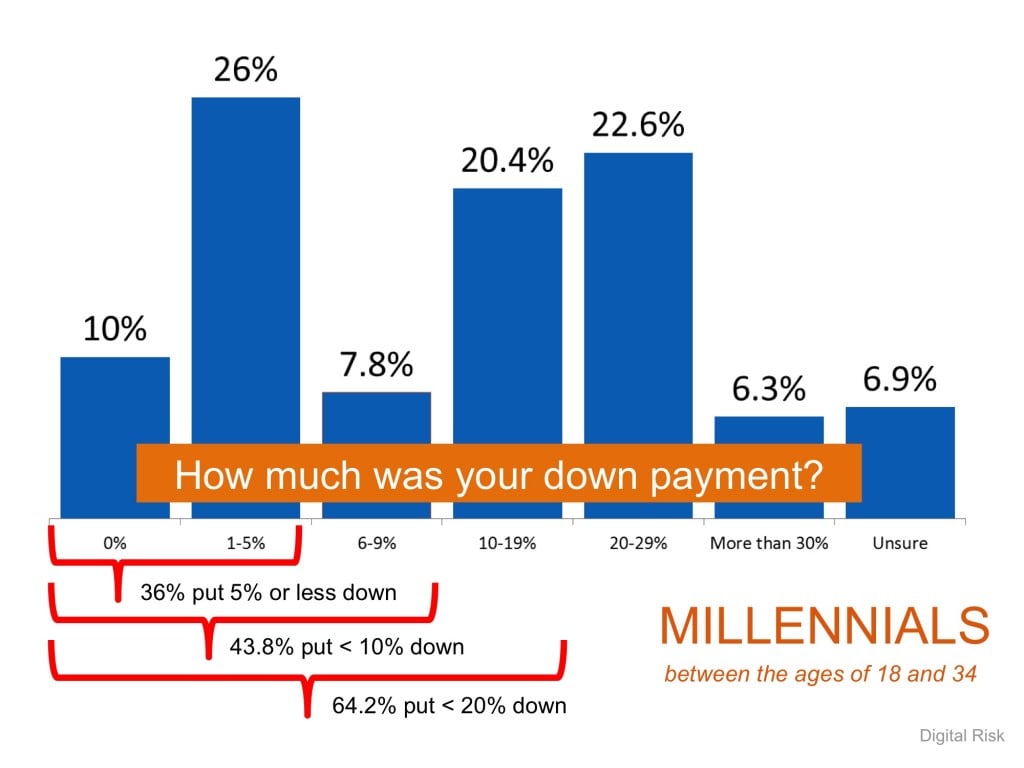

Below are the results of a Digital Risk survey of Millennials who recently purchased a home.

There are some people that have not purchased a home because they are uncomfortable taking on the obligation of a mortgage. Everyone should realize that, unless you are living with your parents rent free, you are paying a mortgage - either yours or your landlord’s.

As The Joint Center for Housing Studies at Harvard University explains:

“Households must consume housing whether they own or rent. Not even accounting for more favorable tax treatment of owning, homeowners pay debt service to pay down their own principal while households that rent pay down the principal of a landlord plus a rate of return.

That’s yet another reason owning often does—as Americans intuit—end up making more financial sense than renting.”

![Want to Get an A? Hire A Real Estate Pro [INFOGRAPHIC] | Simplifying The Market](http://www.simplifyingthemarket.com/wp-content/uploads/2016/08/A-Reasons-To-Use-A-RE-Pro-STM-791x1024.jpg)

![How Supply & Demand Impacts the Real Estate Market [INFOGRAPHIC] | Simplifying The Market](http://www.simplifyingthemarket.com/wp-content/uploads/2016/08/201660826-STM-ENG-653x1024.jpg)