We previously reported how a shortage of inventory in the starter and trade-up home markets is driving prices up and causing bidding wars, creating a true seller’s market. At the same time, in the premium home market, an over-abundance of inventory has started to see prices come down and put buyers in the driver’s seat, creating the beginning of a buyer’s market.

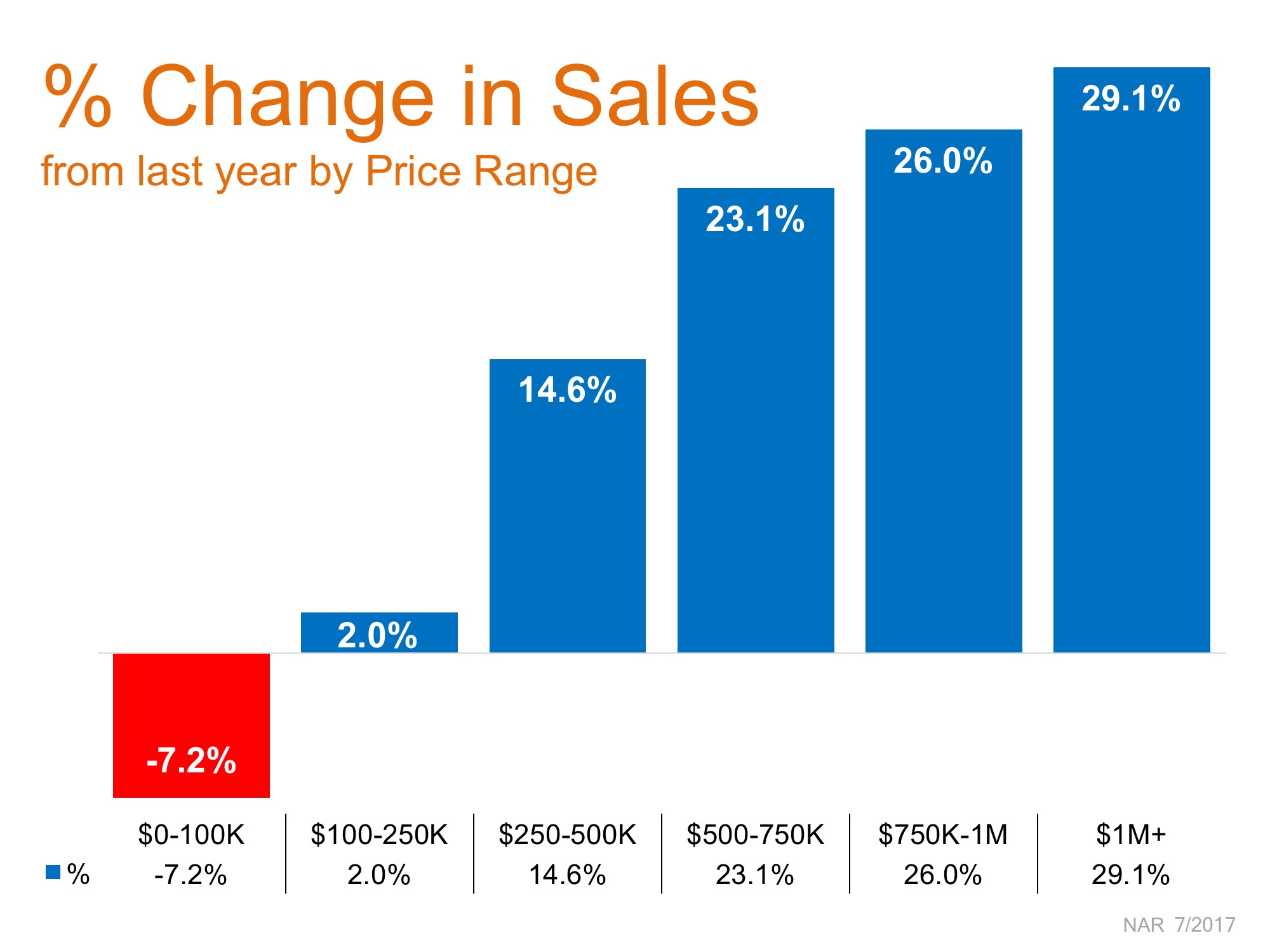

Last week, the National Association of Realtors released their Existing Home Sales Report which shed some additional light on the impact of inventory levels on sales in each price range.

The chart below shows the year-over-year difference in sales at each price range.

The under $100K range has shown declines in recent years due to the shortage of distressed homes available for

When you make an offer on a home, is it a good idea to add an escalation clause? Sometimes they work out but sometimes both the buyer and the seller get burned.

Welcome to another episode of “What’s Working Now!”

Sometimes, buyers will include escalation clauses when they make an offer. Today, I’ll go over the good, the bad, and the ugly when it comes to offers with an escalation clause.

An escalation clause is when the buyer says, “Mr. and Mrs. Seller, I will pay this amount more than any other buyer, but I won’t go higher than this amount.”

What’s the good thing about an escalation clause? As a seller, you may be able to get them up to that higher number.

In many markets across the country, the number of buyers searching for their dream homes greatly outnumbers the amount of homes for sale. This has led to a competitive marketplace where buyers often need to stand out. One way to show you are serious about buying your dream home is to get pre-qualified or pre-approved for a mortgage before starting your search.

Even if you are in a market that is not as competitive, knowing your budget will give you the confidence of knowing if your dream home is within your reach.

Freddie Mac lays out the advantages of pre-approval in the My Home section of their website:

“It’s highly recommended that you work with your lender to get pre-approved before you begin house hunting. Pre-approval will tell you

In Realtor.com’s recent article, “Home Buyers’ Top Mortgage Fears: Which One Scares You?” they mention that “46% of potential home buyers fear they won’t qualify for a mortgage to the point that they don’t even try.”

Myth #1: “I Need a 20% Down Payment”

Buyers overestimate the down payment funds needed to qualify for a home loan. According to the First Quarter 2017 Homeownership Program Index (HPI) from Down Payment Resource, saving for a down payment was the barrier that kept 70% of renters from buying.

Rob Chrane, CEO of Down Payment Resource had this to say,

“There are many mortgage-ready renters today, but they don’t know it. Often, homebuyers remain sidelined for years due to the down payment.”

Spacious one bedroom at the sought after Elizabeth condo. Updated kitchen, wood floors & great closet space. Luxury high rise at Metro with reserved parking, 24-hour front desk, beauty salon/ barber shop, convenience store, exercise room, library, meeting room, newspaper service, party room, indoor pool, sauna spa.

$888.67 per month includes water, sewer, heat, electricity, trash removal, snow removal, professional managmenet, maintenance, lawn care, master insturance policy, reserve fund and all amenities.

Historically, the choice between renting or buying a home has been a tough decision.

Looking at the percentage of income needed to rent a median-priced home today (29.2%) vs. the percentage needed to buy a median-priced home (15.8%), the choice becomes obvious.

Every market is different. Before you renew your lease again, find out if you can put your housing costs to work by buying this year!

Thinking about buying or selling? You probably have questions. CLICK the link below for a free, confidential 17 minute conversation... LET'S TALK!

We often discuss the difference in family wealth between homeowner households and renter households. Much of that difference is the result of the equity buildup that homeowners experience over the time that they own their home. In a report recently released by the nonpartisan Employee Benefit Research Institute (EBRI), they reveal how valuable equity can be in retirement planning.

Craig Copeland, Senior Research Associate at EBRI, recently authored a report, Importance of Individual Account Retirement Plans and Home Equity in Family Total Wealth, in which he reveals:

“Individual account retirement plan assets, plus home equity, represent almost all of what families have to use for retirement expenses outside of Social Security and traditional

Many real estate economists have called on new home builders to ramp up production to help relieve the shortage of inventory of homes for sale throughout the United States. The added inventory would no doubt aid buyers in their search to secure their dream home, while also helping to ease price increases throughout the country.

Unfortunately for builders, there are many forces that are making it difficult for them to do just that!

Last week at the National Association of Real Estate Editors 51st Annual Conference, CoreLogic’s Chief Economist Frank Nothaft broke down the 4 ‘L’s of New Home Construction: Lots, Labor, Lumber, and Lending.

The concept of supply and demand is ripe in the new home construction industry. The four ‘L’s of new home

CoreLogic’s latest Equity Report revealed that 91,000 properties regained equity in the first quarter of 2017. This is great news for the country, as 48.2 million of all mortgaged properties are now in a positive equity situation.

Price Appreciation = Good News for Homeowners

Frank Nothaft, CoreLogic’s Chief Economist, explains:

“One million borrowers achieved positive equity over the last year, which means risk continues to steadily decline as a result of increasing home prices.”

Frank Martell, President and CEO of CoreLogic, believes this is a great sign for the market in 2017 as well, as he had this to say:

“Homeowner equity increased by $766 billion over the last year, the largest increase since Q2 2014. The rising cushion

The results of the latest Rent vs. Buy Report from Trulia show that homeownership remains cheaper than renting with a traditional 30-year fixed rate mortgage in the 100 largest metro areas in the United States.

The updated numbers actually show that the range is an average of 3.5% less expensive in San Jose (CA), all the way up to 50.1% less expensive in Baton Rouge (LA), and 33.1% nationwide!

Other interesting findings in the report include:

Interest rates have remained low and, even though home prices have appreciated around the country, they haven’t greatly outpaced rental appreciation.

With rents & home values moving in tandem, shifts in the ‘rent vs. buy’ decision are largely driven by changes in mortgage interest rates.

![The Cost of Renting vs. Buying in the US [INFOGRAPHIC] | Simplifying The Market](http://d39ah2zlibpm3g.cloudfront.net/wp-content/uploads/2017/06/20140248/20170623-Rent-vs.-Buy-STM.jpg)

.jpg)