The Cost of Waiting to Buy is defined as the additional funds it would take to buy a home if prices & interest rates were to increase over a period of time.

Freddie Mac predicts interest rates to rise to 4.6% by next year.

CoreLogic predicts home prices to appreciate by 5.3% over the next 12 months.

If you are ready and willing to buy your dream home, find out if you are able to!

Whether you are considering the purchase of your first home or trading up to the home your family frequently fantasizes about, there are three crucial questions you must know the answer to:

What is the minimum down payment required to purchase a home?

What is the minimum FICOscore required to qualify for a mortgage?

What is the maximum Back-End DTI Ratio allowed?

A survey conducted by Fannie Mae revealed startling information: most Americans don’t know the answer to these three crucially important questions. Here is a graphic showing the results of the survey:

The percentages are quite disturbing but can explain why so many people believe they are not eligible to purchase a home whether it is a first home or

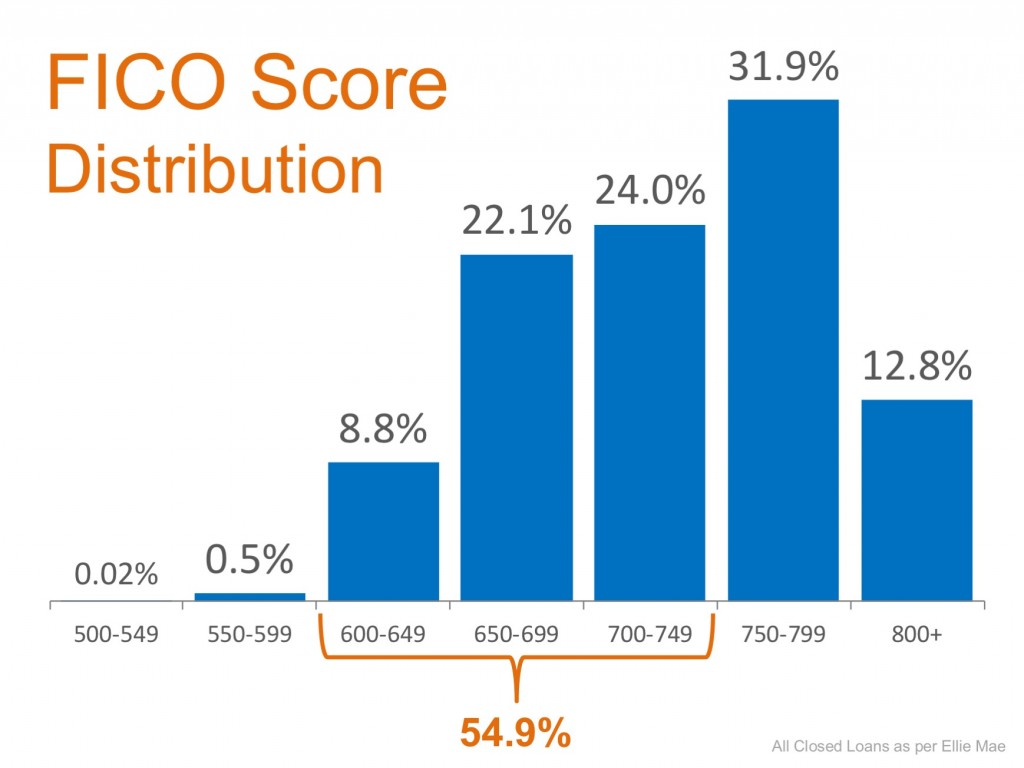

The widespread myth that perfect credit and large down payments are necessary to buy a home are holding many potential home buyers on the sidelines. According to Ellie Mae’s latest Origination Report, the average FICO score for all closed loans in May was 724, far lower than the 750 or 800 that many buyers believe to be true.

Below is a graph of the distribution of FICO scores of approved loans in May (the latest available data):

Looking at the chart above, it becomes obvious that not only do you not need a 750+ credit score, but 54.9% of approved loans actually had a score between 600 and 749.

More and more experts are speaking up about the fact that if potential buyers realized they could be approved for a mortgage with a credit score

The most recent Housing Pulse Survey released by the National Association of Realtors revealed that the two major reasons Americans prefer owning their own home instead of renting are:

They want the opportunity to build equity.

They want a stable and safe environment.

Building Equity

John Taylor, CEO of the National Community Reinvestment Coalition, explains that those who lack the opportunity to become homeowners have a weakened ability to reinvest their wealth:

“We traditionally have been huge supporters of homeownership. We see it as a way to provide stability for households but also as an asset-building strategy. If you continue to be a renter, locked out of the homeownership arena, increasingly those things are further and

As a seller, you will be most concerned with the ‘short term price’ – where home values are headed over the next six months. As a buyer, you must be concerned not with price but instead with the ‘long term cost’ of the home.

Many economists have pointed to Brexit (Britain’s exit from the European Union) as a reason that interest rates will remain low for the next few months. But Trulia’s Chief Economist Ralph McLaughlin warns that this will not always be the case in a recent post:

“While the departure of the UK from the European Union has driven down the 10-year bond, and thus mortgage rates, we expect them to rebound later in the year as uncertainty over the economic consequences of the departure lifts.”

I'm going to tell you about my latest marketing innovation... 'Moving Pictures.' You won't believe what happened at my open house!

My husband, Bill, and I were in an Uber on our way home from Reagan National Airport. My phone rang. It was Carol.

'Marjorie, I have a friend who needs your help. She's getting ready to put her house on the market with another agent, and I'm afraid she's making a terrible mistake!'

'Carol, of course I'll help. How can I reach her?'

'She's right here with me, I'm handing her my phone.'

So that's how I met Christine! To make a long story short, she hired me and we introduced the world to personalized 'Moving

Last week, the National Association of Realtors (NAR) released their Pending Home Sales Index, a forward-looking indicator of home sales based on contract signings. The report revealed that this May’s numbers weren’t quite as good as the year before:

“With last month’s decline, the index reading is still the third highest in the past year, but declined year-over-year for the first time since August 2014.”

The mainstream media ran headlines highlighting that the index had dropped for the first time in two years. Many read this as an indication that the housing market must be slowing down.

If you were thinking that now may be the perfect time to put your house on the market, these reports may have caused you some concern. We want to

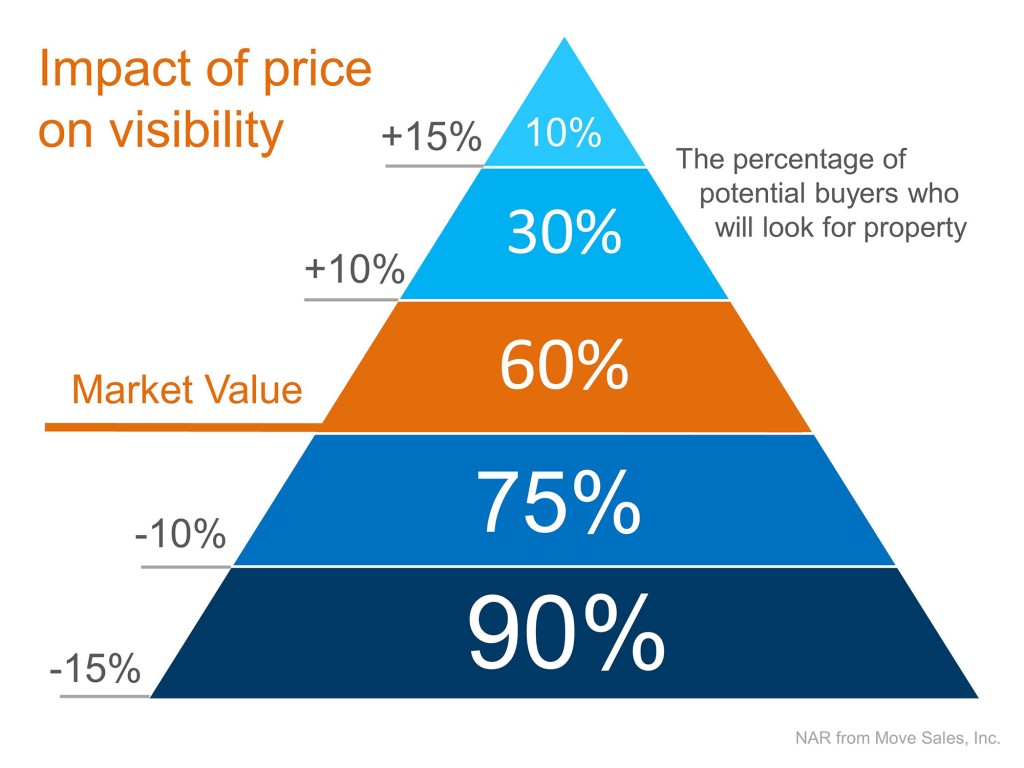

Every homeowner wants to make sure they get the best price when selling their home. But how do you guarantee that you receive maximum value for your house? Here are two keys to ensuring you get the highest price possible.

1. Price it a LITTLE LOW

This may seem counterintuitive. However, let’s look at this concept for a moment. Many homeowners think that pricing their home a little OVER market value will leave them room for negotiation. In actuality, this just dramatically lessens the demand for your house (see chart below).

Instead of the seller trying to ‘win’ the negotiation with one buyer, they should price it so that demand for the home is maximized. In that way, the seller will not be fighting with a buyer over the price, but instead

Summer is here! The temperature isn't the only thing heating up right now, so too is the housing market in many areas of the country! Here are four great reasons to consider buying a home today instead of waiting.

1. Prices Will Continue to Rise

CoreLogic’s latest Home Price Index reports that home prices have appreciated by 6.2% over the last 12 months. The same report predicts that prices will continue to increase at a rate of 5.3% over the next year. The Home Price Expectation Survey polls a distinguished panel of over 100 economists, investment strategists, and housing market analysts. Their most recent report projects home values to appreciate by more than 3.2% a year for the next 5 years.

![Should I Wait Until Next Year? Or Buy Now? [INFOGRAPHIC] | Simplifying The Market](http://www.simplifyingthemarket.com/wp-content/uploads/2016/07/Cost-of-Waiting-STM-791x1024.jpg)

![Saving To Buy A Home? What Would You Sacrifice? [INFOGRAPHIC] | Simplifying The Market](http://www.simplifyingthemarket.com/wp-content/uploads/2016/07/Sacrifices-to-Buy-BOA-STM-791x1024.jpg)