Over the next five years, home prices are expected to appreciate 3.24% per year on average and to grow by 21.4% cumulatively, according to Pulsenomics’ most recent Home Price Expectation Survey.

So, what does this mean for homeowners and their equity position?

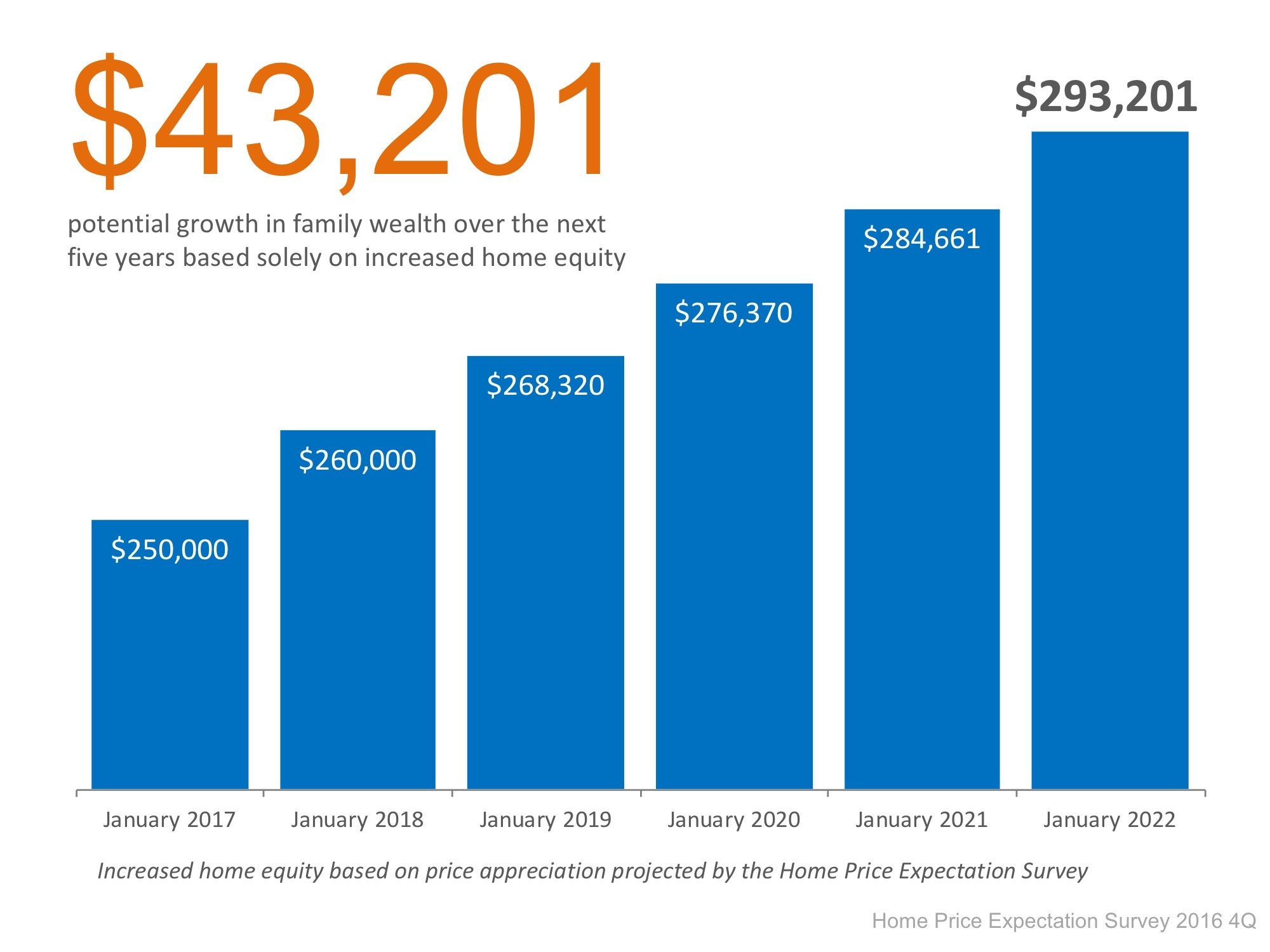

As an example, let’s assume a young couple purchases and closes on a $250,000 home in January. If we look at only the projected increase in the price of that home, how much equity will they earn over the next 5 years?

Since the experts predict that home prices will increase by 4.0% this year alone, the young homeowners will have gained over $10,000 in equity in just one year.

Over a five-year period, their equity will increase by over $43,000! This figure does not even take into

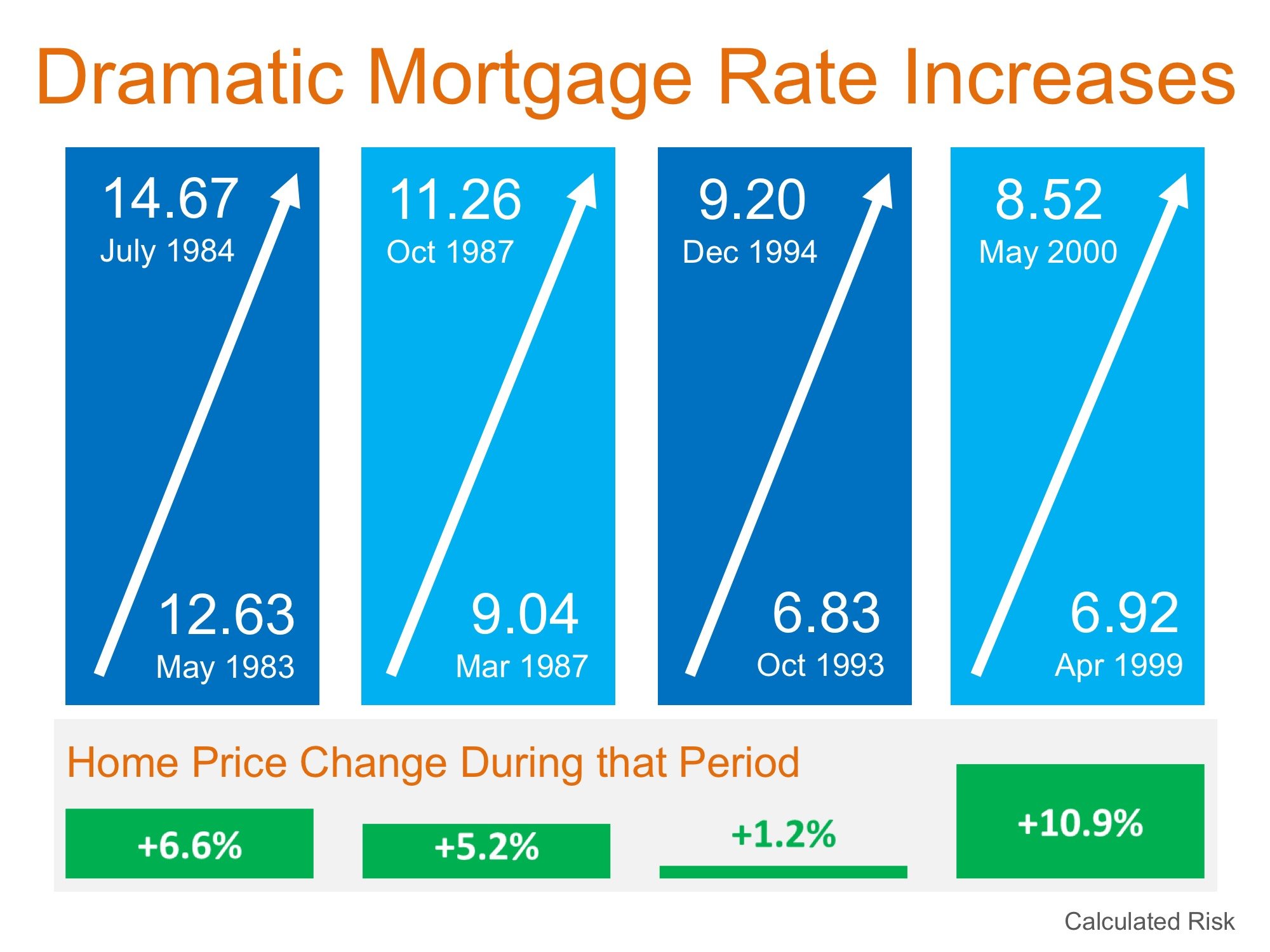

There are some who are calling for a decrease in home prices should mortgage interest rates begin to rise rapidly. Intuitively, this makes sense as the cost of a home is determined by the price of the home, plus the cost of financing that home. If mortgage interest rates increase, fewer people will be able to buy, and logic says prices will fall if demand decreases.

However, history shows us that this has not been the case the last four times mortgage interest rates dramatically increased.

Here is a graph showing what actually happened:

Last week, in an article titled “Higher Rates Don’t Mean Lower House Prices After All,” the Wall Street Journal revealed that a recent study by John Burns Real Estate Consulting Inc. found that:

A recent study of more than 7 million home sales over the past four years revealed that the season in which a home is listed may be able to shed some light on the likelihood that the home will sell for more than asking price, as well as how quickly the sale will close.

It’s no surprise that listing a home for sale during the spring saw the largest return, as the spring is traditionally the busiest month for real estate. What is surprising, though, is that listing during the winter came in second!

“Among spring listings, 18.7 percent of homes fetched above asking, with winter listings not far behind at 17.5 percent. While 48.0 percent of homes listed in spring sold within 30 days, 46.2 percent of homes in winter did the same.”

People often ask if now is a good time to buy a home. No one ever asks when a good time to rent is. However, we want to make certain that everyone understands that today is NOT a good time to rent.

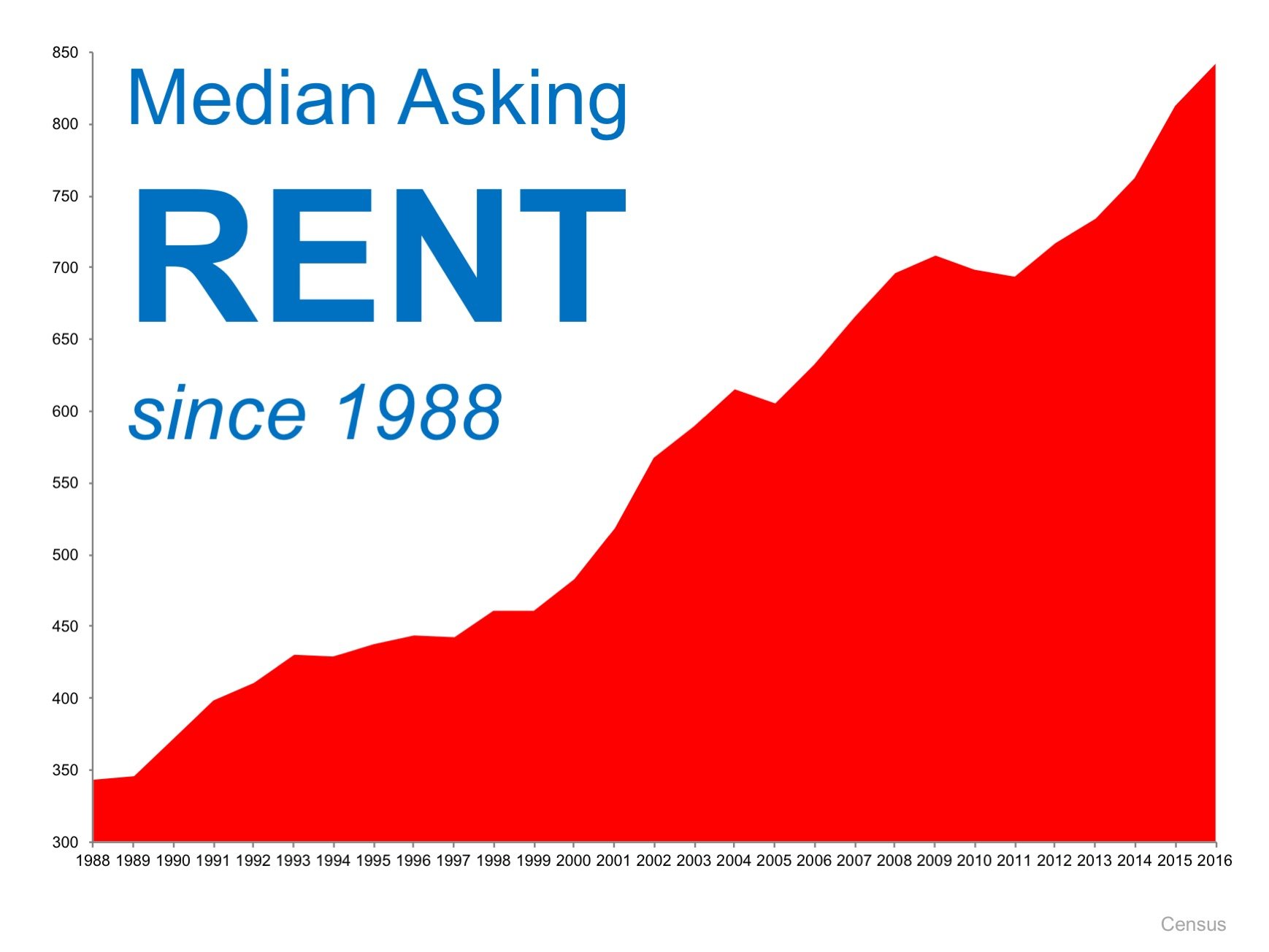

The Census Bureau recently released their third quarter median rent numbers. Here is a graph showing rent increases from 1988 until today:

As you can see, rents have steadily increased and are showing no signs of slowing down. If you are faced with the decision of whether you should renew your lease or not, you might be pleasantly surprised at your ability to buy a home of your own instead.

Bottom Line

One way to protect yourself from rising rents is to lock in your housing expense by buying a home. If you are ready and willing to buy, let’s

Welcome to the latest episode of What’s Working Now!

Today we’re answering a question from Bob, who’s curious about planning ahead when selling your home. Bob asks, “What repairs, improvements, etc. should be made in order to get the best return later?”

In my previous videos, I covered how to update the walls and floors of your home, as well as how to begin the home improvement process. Today, I am going to expand on the two most important rooms that you should focus on upgrading in order to get the highest return on your investment: the kitchen and master bathroom.

First, let’s start with the kitchen. Depending on how large your home is or how many improvements you need, improving the kitchen could mean just changing

As the temperature in many areas of the country starts to cool down, you might think that the housing market will do the same. This couldn’t be further from the truth! Here are 4 reasons you should consider buying your dream home this winter instead of waiting for spring!

1. Prices Will Continue to Rise

CoreLogic’s latest Home Price Index reports that home prices have appreciated by 6.3% over the last 12 months. The same report predicts that prices will continue to increase at a rate of 5.2% over the next year.

The bottom in home prices has come and gone. Home values will continue to appreciate for years. Waiting no longer makes sense.

2. Mortgage Interest Rates are Projected to Increase

Updated semi-detached home with 4 bedrooms, 2 full baths and huge front porch. Large kitchen with granite counters, living room, formal dining room with french doors to sunroom/den opens to back deck and deep, landscaped yard. High ceilings, moldings, large windows, wood floors & central A/C. Unbeatable location! Steps to Metro, movies, shops and grocery.

Visit www.3922Livingston.com to view architectural photos and full color floor plan.

According to a recent report by Trulia, “buying is cheaper than renting in 100 of the largest metro areas by an average of 37.7%.” That may have some thinking about buying a home instead of signing another lease extension. But, does that make sense from a financial perspective?

In the report, Ralph McLaughlin, Trulia’s Chief Economist explains:

“Owning a home is one of the most common ways households build long-term wealth, as it acts like a forced savings account. Instead of paying your landlord, you can pay yourself in the long run through paying down a mortgage on a house.”

The report listed five reasons why owning a home makes financial sense:

![Americans Are on The Move [INFOGRAPHIC] | Simplifying The Market](http://www.simplifyingthemarket.com/wp-content/uploads/2016/12/MovingAcrossAmerica2016-STM.jpg)