According to a Merrill Lynch study, “an estimated 4.2 million retirees moved into a new home last year alone.” Two-thirds of retirees say that they are likely to move at least once during retirement.

As one participant in the study stated:

“In retirement, you have the chance to live anywhere you want. Or you can just stay where you are. There hasn’t been another time in life when we’ve had that kind of freedom.”

The top reason to relocate cited was “wanting to be closer to family” at 29%, a close second was “wanting to reduce home expenses” at 26%.

A recent Freddie Mac study found similar results, as “nearly 20 percent of Boomers said they would move closer to their grandchildren/children compared to 13 percent who said they would

The Consumer Price Index (CPI) was released by the Labor Department last week. An analysis by Market Watch revealed the cost of rent was 3.8% higher than a year ago for the second straight month in June. That’s the strongest yearly price gain since 2007.

This coincides with a report released earlier this month in which AxioMetrics announced that rents are continuing to increase in 2016. The report revealed:

There was a 3.7% increase in effective rents in the second quarter of 2016 as compared to the same period last year.

That the effective rent growth this quarter compared to last quarter was 2.3%.

Annual effective rent growth was positive in 49 of the top 50 markets, based on number of units. Only Houston was negative, at -1.4%, as

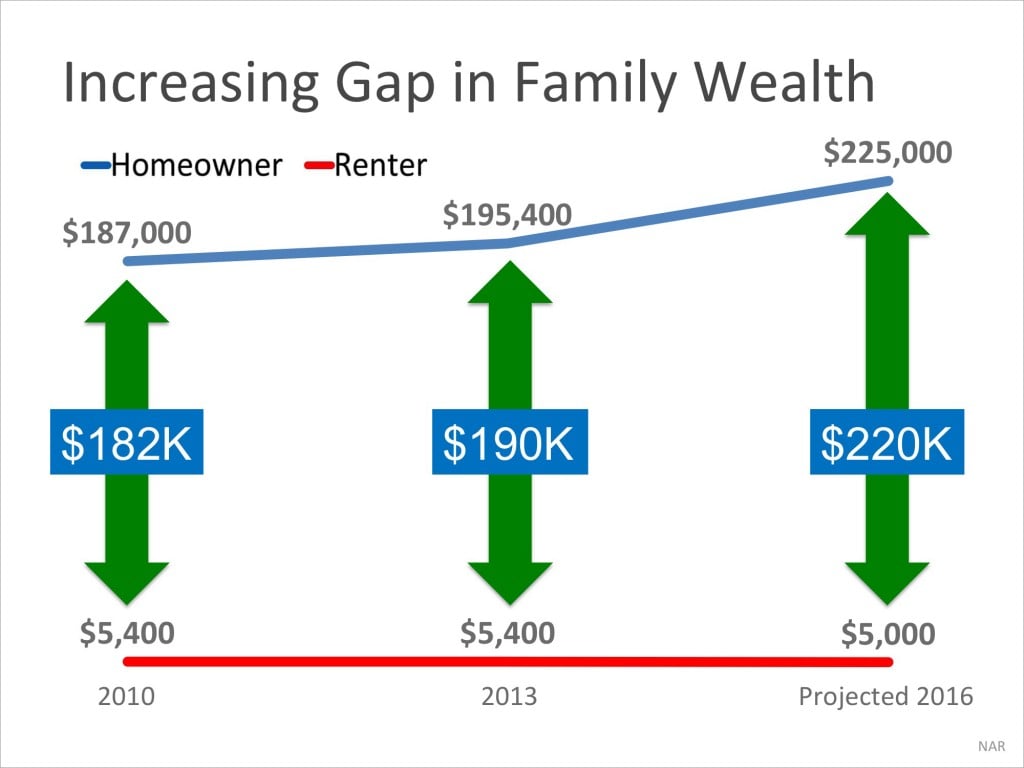

Every three years, the Federal Reserve conducts a Survey of Consumer Finances in which they collect data across all economic and social groups. The latest survey, which includes data from 2010-2013, reports that a homeowner’s net worth is 36 times greater than that of a renter ($194,500 vs. $5,400).

In a Forbes article, the National Association of Realtors’ (NAR) Chief Economist Lawrence Yun predicts that in 2016 the net worth gap will widen even further to 45 times greater.

The graph below demonstrates the results of the last two Federal Reserve studies and Yun’s prediction:

Put Your Housing Cost to Work for You

Simply put, homeownership is a form of ‘forced savings.’ Every time you pay your mortgage, you are contributing to your

In one of the nations hottest housing markets, which is home to thousands of real estate agents, arriving at a list of 101 names was no simple feat. First, we surveyed nearly 50,000 local Washingtonian subscribers, plus the more than 1,000 agents who made last year's Best Agents and Top Producers lists.

We asked both groups whom they most enjoyed working with, based on a number of criteria including market knowledge,integrity, communication skills, and closing preparation.

We further vetted those results by contacting still more real estate industry professionals, among them mortgage brokers, additional agents, and home inspectors. For those house-hunting in particular, we've included neighborhoods where

If you are debating purchasing a home right now, you are probably getting a lot of advice. Though your friends and family will have your best interest at heart, they may not be fully aware of your needs and what is currently happening in the real estate market.

Answering the following 3 questions will help you determine if now is actually a good time for you to buy in today’s market.

1. Why am I buying a home in the first place?

This truly is the most important question to answer. Forget the finances for a minute. Why did you even begin to consider purchasing a home? For most, the reason has nothing to do with money.

For example, a recent survey by Braun showed that over 75% of parents say “their child’s education is an important part of

The Cost of Waiting to Buy is defined as the additional funds it would take to buy a home if prices & interest rates were to increase over a period of time.

Freddie Mac predicts interest rates to rise to 4.6% by next year.

CoreLogic predicts home prices to appreciate by 5.3% over the next 12 months.

If you are ready and willing to buy your dream home, find out if you are able to!

Whether you are considering the purchase of your first home or trading up to the home your family frequently fantasizes about, there are three crucial questions you must know the answer to:

What is the minimum down payment required to purchase a home?

What is the minimum FICOscore required to qualify for a mortgage?

What is the maximum Back-End DTI Ratio allowed?

A survey conducted by Fannie Mae revealed startling information: most Americans don’t know the answer to these three crucially important questions. Here is a graphic showing the results of the survey:

The percentages are quite disturbing but can explain why so many people believe they are not eligible to purchase a home whether it is a first home or

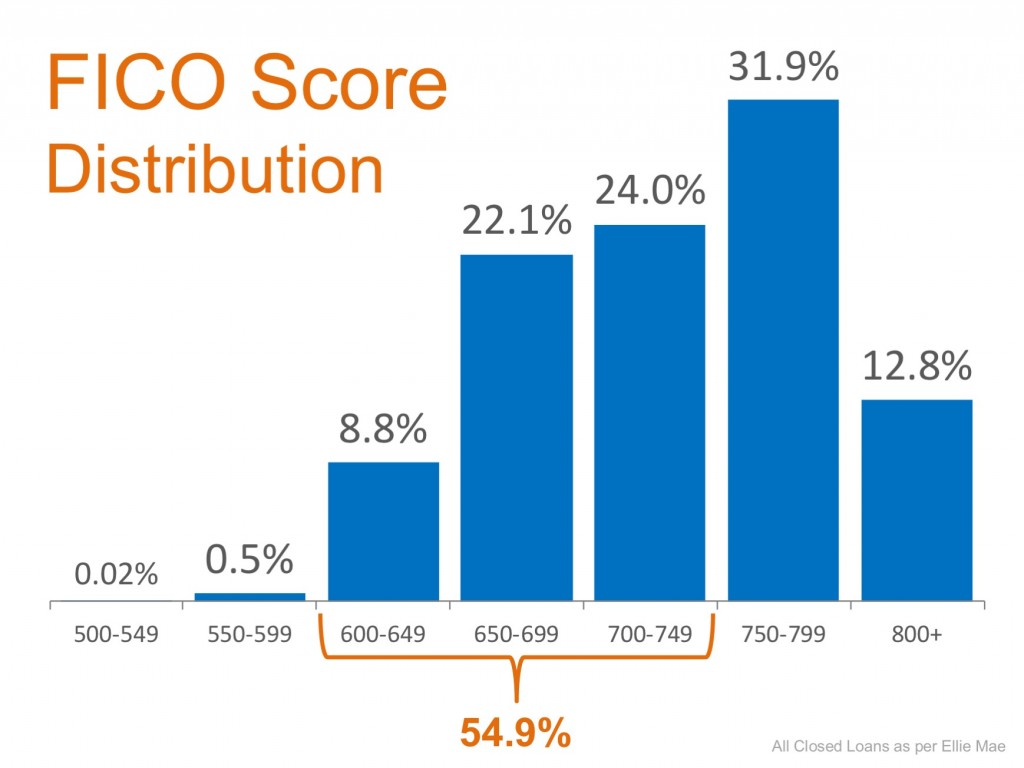

The widespread myth that perfect credit and large down payments are necessary to buy a home are holding many potential home buyers on the sidelines. According to Ellie Mae’s latest Origination Report, the average FICO score for all closed loans in May was 724, far lower than the 750 or 800 that many buyers believe to be true.

Below is a graph of the distribution of FICO scores of approved loans in May (the latest available data):

Looking at the chart above, it becomes obvious that not only do you not need a 750+ credit score, but 54.9% of approved loans actually had a score between 600 and 749.

More and more experts are speaking up about the fact that if potential buyers realized they could be approved for a mortgage with a credit score

The most recent Housing Pulse Survey released by the National Association of Realtors revealed that the two major reasons Americans prefer owning their own home instead of renting are:

They want the opportunity to build equity.

They want a stable and safe environment.

Building Equity

John Taylor, CEO of the National Community Reinvestment Coalition, explains that those who lack the opportunity to become homeowners have a weakened ability to reinvest their wealth:

“We traditionally have been huge supporters of homeownership. We see it as a way to provide stability for households but also as an asset-building strategy. If you continue to be a renter, locked out of the homeownership arena, increasingly those things are further and

As a seller, you will be most concerned with the ‘short term price’ – where home values are headed over the next six months. As a buyer, you must be concerned not with price but instead with the ‘long term cost’ of the home.

Many economists have pointed to Brexit (Britain’s exit from the European Union) as a reason that interest rates will remain low for the next few months. But Trulia’s Chief Economist Ralph McLaughlin warns that this will not always be the case in a recent post:

“While the departure of the UK from the European Union has driven down the 10-year bond, and thus mortgage rates, we expect them to rebound later in the year as uncertainty over the economic consequences of the departure lifts.”

![Should I Wait Until Next Year? Or Buy Now? [INFOGRAPHIC] | Simplifying The Market](http://www.simplifyingthemarket.com/wp-content/uploads/2016/07/Cost-of-Waiting-STM-791x1024.jpg)